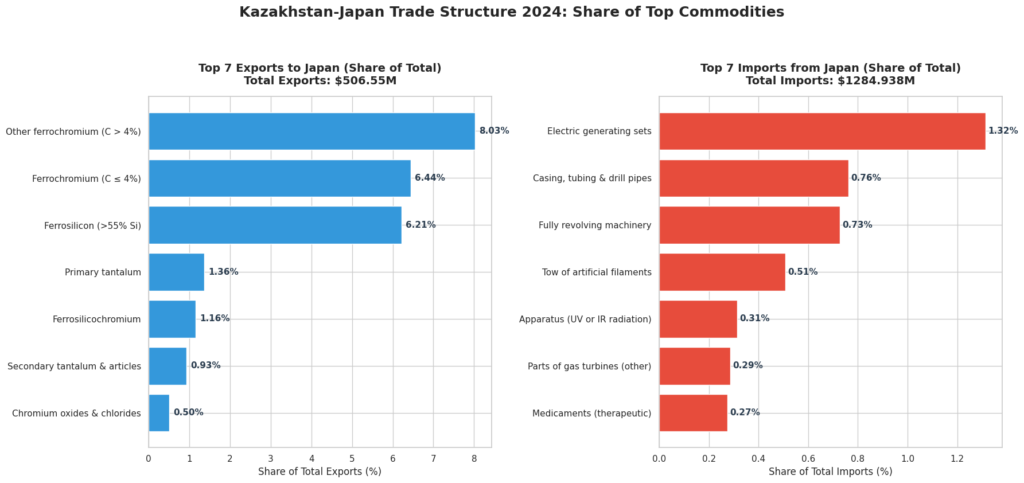

In China’s Shadow: Japan’s Risky Bet on Central Asia’s Resources

Japan is not a newcomer to the rare earth metals market in Central Asia. In fact, its initial entry into the region was a forced reaction to the suspension of Chinese REM exports, a situation that mirrors current geopolitical trends. However, in the mid-2010s, Japanese activity came to a sharp halt, which effectively allowed China to cement its dominance in this sector.

Kazakh expert Rassul Kospanov notes that this was facilitated by a complex set of factors: from a partial restoration of relations between Tokyo and Beijing to economic miscalculations and the failed experience of early joint projects.

Crisis Provokes Interest in Central Asian Resources, Again

The decline of Japanese activity in the Central Asian rare earth metals sphere happened gradually, starting in the mid-2010s. The turning point in REM cooperation was the failed case of the project in Stepnogorsk, Northern Kazakhstan.

While often viewed as a reaction to the 2010 crisis, Japan had actually initiated diversification efforts earlier. The groundwork for the Stepnogorsk facility was laid through a 2009 agreement/MoU on a rare earth recovery project between Sumitomo and Kazatomprom, formalized as the Summit Atom Rare Earth Company (SARECO) joint venture in March 2010. However, the project gained critical strategic urgency following the “Chinese trawler incident” near the disputed Senkaku Islands in September 2010.

At that time, China dominated the mining and processing of rare earth elements, while Japan was one of their largest consumers. Practically speaking, the country had no alternative sources of supply.

The aftermath of the incident remains a subject of debate. Contemporary reports alleged an “unofficial embargo” by Beijing, causing panic and price spikes. However, later analyses of trade statistics suggest exports were not technically “suspended”; dips were short-lived and aligned with China’s pre-announced global quota reductions. Nevertheless, even if the “ban” was unofficial or merely a bureaucratic bottleneck, it acted as a catalyst. The perceived vulnerability compelled Tokyo to fundamentally overhaul its supply chain strategies.

In this context, SARECO, tasked with extracting dysprosium from uranium residue, became a flagship initiative. The plant opened in November 2012 and was eventually expected to supply around 10% of Japan’s annual dysprosium needs, or 50–55 tons.

Kazakh Projects Lost Relevance Following China’s Return

Despite this start, the project quickly “stalled.” Specialists were unable to establish chemical purification of local uranium to Japanese purity standards, and the product contained impurities unacceptable for the automotive and electronics industries. Instead of the originally planned high-margin exports to the Japanese market, SARECO’s production was reoriented toward supplies for Russian enterprises.

Furthermore, after 2014, prices began to decline. Chinese suppliers returned to the global market following a WTO ruling that declared Beijing’s export restrictions illegal, and they managed to sharply reduce production costs.

As a result, alternative projects outside of China, including the one in Stepnogorsk, lost their economic attractiveness. By 2015, the project was effectively frozen without ever reaching an industrial scale.

Simultaneously, Japan successfully pivoted to other alternatives, such as the Lynas project in Australia and advanced recycling technologies. By the 2020s, Japan’s reliance on Chinese imports dropped from over 90% to around 58%, effectively reducing the immediate urgency for Central Asian projects at that time.

Why Is It Important for Japan to Return to Central Asia Today?

For Japan’s high-tech economy, rare earth metals are a critical factor in industrial and technological security, especially amidst growing geopolitical turbulence and the persistent concentration of REM mining and processing in China.

Beijing’s dominant position in the rare earth market, supplemented by its active investment presence in Central Asia, increases the vulnerability of alternative supply chains and heightens the significance of the C5 nations capable of providing diversification. In this configuration, it is vital for Japan to possess “backup” supply chains. This means not just purchasing agreements, but long-term offtakes, equity stakes in projects, and its own geological exploration base in the region.

The Stepnogorsk experience, when Japanese activity in the region was reactive and short-term, demonstrated the shortsightedness of a tactical approach that lacks the construction of sustainable value chains. Since 2022, a queue of investors willing to invest in the Central Asian REM industry has formed in the region.

Today, Japan lags behind other actors (China, Russia, France, and South Korea) in economic activity on the Central Asian track; these competitors are entering projects faster and ramping up their industrial presence more actively. For instance, this summer, France’s Orano announced a $214 million investment in uranium mining at the South Djengeldi deposit in Uzbekistan.

Meanwhile, American firm Cove Capital announced the creation of a joint venture to develop a tungsten deposit in Central Kazakhstan, with an investment volume expected to exceed $1 billion.

The C5 states traditionally remain open to foreign investors. Undoubtedly, certain bureaucratic and institutional peculiarities persist in the region; however, it must be acknowledged that Central Asian countries are generally interested in attracting Japanese capital and technology.

These nations are actively providing foreign capital with access to critical metals. In this logic, for Tokyo, which might have a desire to reduce Chinese and Russian influence in the region, Central Asia represents a favorable opportunity to secure a foothold in the REM sector by combining economic pragmatism with the objectives of geopolitical diversification.

Outlook

At the same time, there are already successful examples of Japanese presence in Central Asia, primarily the APPAK joint venture in the Turkestan region. This asset, involving Kazatomprom, Sumitomo Corporation, and Kansai Electric Power, reached industrial levels long ago and operates a full production cycle in the uranium industry.

This case clearly demonstrates that Japanese projects can be sustainable given a long investment horizon. In the past, Japanese activity in the REM sector was situational and was rolled back against the backdrop of falling prices, Chinese dominance, and high technological complexity. However, today’s geopolitical climate and the rising demand for critical metals are changing the rules of the game.

Under these circumstances, a Japanese return to Central Asia is possible and justified only in a strategic format with long-term investments, geological exploration, and entrenched positions in projects because otherwise, the niche will be occupied by more active competitors.